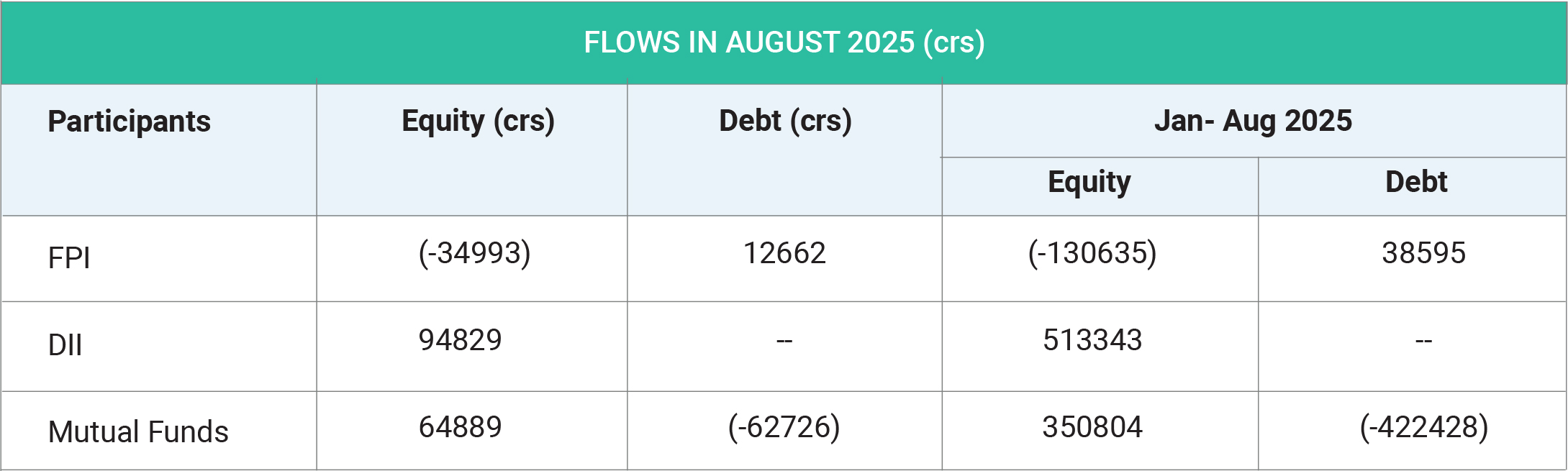

In August 2025, the Indian equity markets experienced a month characterized by modest headline gains but significant underlying volatility, as the Sensex and Nifty 50 reflected a tug-of-war between adverse global events, heavy foreign outflows, and supportive domestic developments. The Sensex largely hovered near the crucial 80,000 mark and closed at 80,718 on September 4, registering a marginal uptick of just 0.01%, while the Nifty 50 ended at around 24,735, showing a similarly muted advance of approximately 0.08%, and although these percentage gains were minimal, the real story of the month was the sharp intra-day swings and sectoral churn that kept investors on edge. Notably, indices witnessed abrupt declines of nearly 1% on August 8 and

26, reflecting fragile sentiment and investor risk aversion amid mounting concerns over global trade tensions and currency depreciation, reacting sharply to any adverse headlines. The primary catalyst for this heightened volatility was the escalation of trade tensions between India and the United States, as tariff threats hung heavily over market sentiment throughout the month, culminating in Washington’s decision on August 27 to impose a steep 50% tariff on Indian goods, doubling the earlier 25% rate set in July, in response to India’s purchase of discounted Russian oil. This move directly targeted critical export sectors such as gems and jewellery, textiles, footwear, and industrial chemicals, sparking fears that Indian exports to the US could contract by as much as 43%, triggering sharp selloffs across related sectors and accelerating foreign institutional investor (FII) exits. As a result, FIIs remained persistent net sellers throughout the month, withdrawing an estimated ₹47,000 crore from Indian equities, citing not only tariff fears but also the backdrop of a strengthening US dollar, elevated global bond yields, and lingering uncertainty over US economic policy. Export-oriented industries like IT, pharmaceuticals, and specialty chemicals bore the brunt of this selling, dragging down valuations and leading to broader corrections across the benchmark indices. These sustained FII outflows also placed downward pressure on the rupee, which slid close to an all-time low of ₹87.66 per dollar on August 4, adding another layer of vulnerability to sectors dependent on imports and further denting market confidence. Yet, despite this pronounced external weakness, the Indian market avoided a steeper correction thanks to the robust counterbalancing role played by domestic institutional investors (DIIs), who acted as shock absorbers during turbulent phases. DIIs, including mutual funds, LIC, and insurance companies, injected a massive ₹95,000 crore into equities during the month, nearly double the amount withdrawn by FIIs, and this strong domestic buying, focused particularly on fundamentally sound sectors like banking, infrastructure, and consumer goods, helped cushion the indices against deeper falls. These capital flow dynamics, sectoral performances were uneven, with auto and FMCG sectors delivering robust gains driven by healthy domestic sales and resilient consumption demand, while pharma, financials, and defence counters came under pressure due to global headwinds and tariff uncertainties. The market was influenced by phases of profit-booking, as investors locked in early-August gains from heavyweight stocks, occasionally pushing indices into negative territory, though recoveries were often aided by positive domestic policy moves. One of the most significant domestic policy developments was the Group of Ministers’ approval on August 21 of a major simplification in the Goods and Services Tax (GST) structure, which proposed merging most rates into two slabs of 5% and 18% with expected implementation by late September. This reform was interpreted as a potential consumption booster ahead of the festive season, benefiting consumer-focused sectors and fuelling optimism that supported markets during an otherwise challenging month. In contrast, another notable domestic move—the passing of the Promotion and Regulation of Online Gaming Bill, 2025, which imposed a complete ban on real-money online gaming—negatively impacted listed entities in the digital gaming space, showing the divergent effects of sector-specific policy. Macroeconomic indicators also provided resilience: India’s GDP growth was projected at a strong 6.5% for FY25, while the services sector PMI reached a 15-year high of 62.9 in August, signalling robust expansion in domestic services activity. Inflation, meanwhile, remained subdued, with even food inflation turning negative, supporting rural consumption and bolstering the outlook for consumer demand. The Reserve Bank of India maintained its accommodative stance, keeping the repo rate steady at 5.5% while ensuring liquidity and credit flow, with the benign inflation backdrop giving policymakers room to support growth without stoking inflationary pressures. Export performance too remained encouraging in certain areas, as shipments rose nearly 6% year-on-year in Q1 FY26, aided by government initiatives like the Foreign Trade Policy 2023 and the Make in India program, which particularly boosted electronics competitiveness. On the global front, in addition to tariff escalations, other developments also weighed on Indian equities: persistently high global interest rates in the US and EU constrained liquidity and kept capital flows under pressure, while muted global growth forecasts from the IMF and World Bank underscored weakening demand in key export markets such as the US, EU, UK, and Germany, particularly hurting India’s IT, textile, and pharmaceutical sectors. At the same time, the Jackson Hole Economic Symposium provided a temporary boost to sentiment when the US Federal Reserve Chair hinted at the possibility of rate cuts in the near future, offering hope of eventual liquidity easing. Nevertheless, the net effect of global events remained heavily skewed toward caution, as evidenced by FII outflows exceeding ₹35,000 crore during the month, largely in response to trade tariffs, weak global demand, and rupee depreciation. Overall, August 2025 was a month of contrasts for Indian markets: on one side, heavy foreign selling, tariff shocks, rupee weakness, and global uncertainty drove sharp volatility and tested investor nerves, while on the other, strong domestic inflows, policy reforms like GST simplification, resilient macroeconomic data, and sectoral bright spots in autos, FMCG, and banking prevented steep corrections and kept benchmarks range-bound. The broader implication was that the Indian market demonstrated increasing resilience against global shocks, as domestic liquidity and retail participation emerged as decisive stabilizers. The August narrative highlighted the evolving balance of power between FIIs and DIIs, the vulnerability of export-oriented sectors to external shocks, the growing importance of domestic consumption in sustaining momentum, and the capacity of policy reforms to shape investor sentiment, making the month a vivid case study in how external turbulence and internal resilience can coexist to define the trajectory of India’s financial markets.

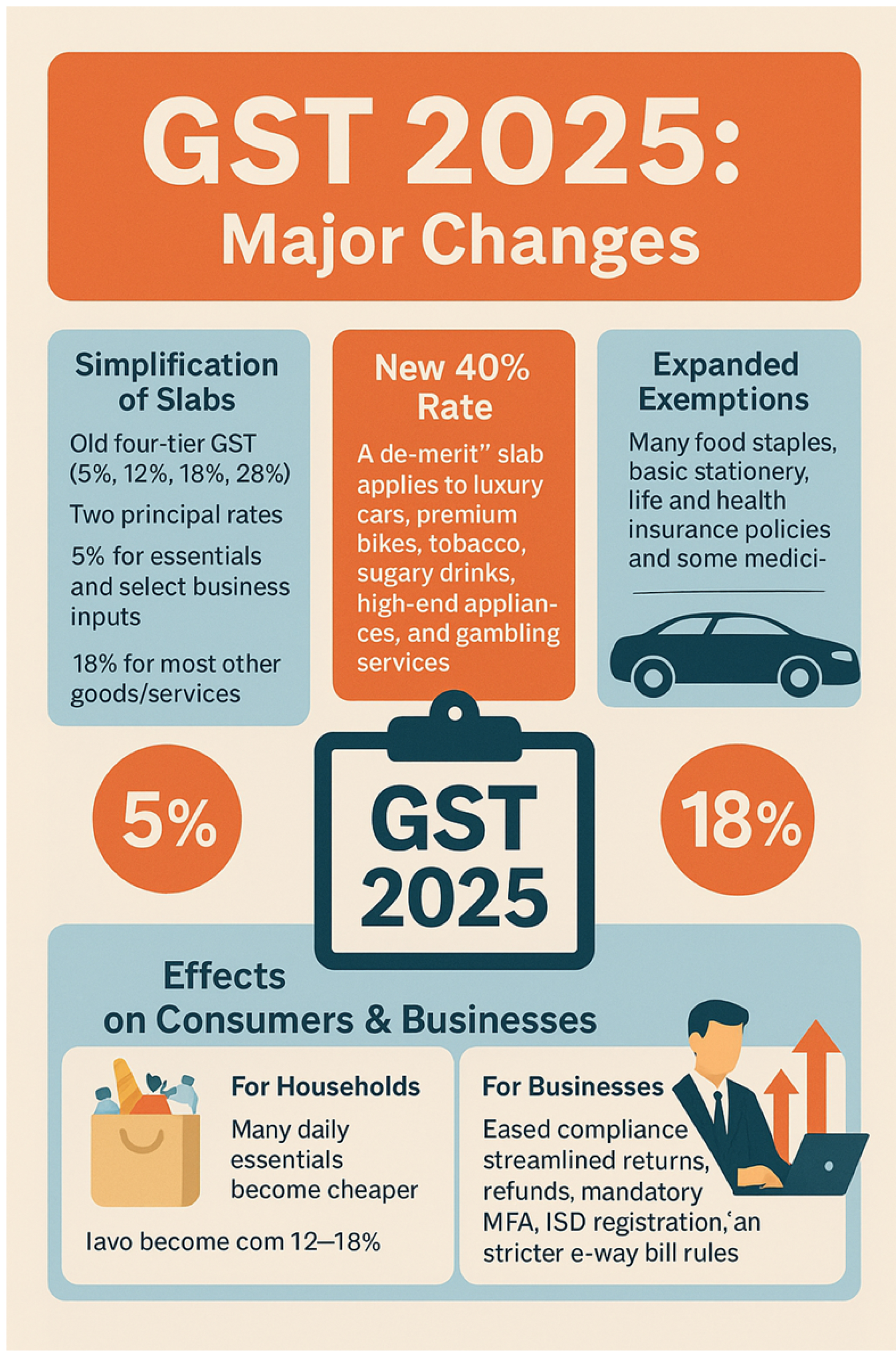

In August 2025, the Indian debt market presented a nuanced picture of resilience balanced against pressure, as yields across maturities moved upward in response to fiscal and demand concerns, yet remained broadly stable due to steady foreign inflows and supportive domestic liquidity measures, making the month a study in contrasts between global headwinds and local stabilizers. The benchmark 10-year government bond yield, which had hovered in a narrow range of 6.55% to 6.56% earlier in the month, ultimately surged by nearly 24 basis points to end closer to 6.62%, while the 30-year government bond yield climbed even more dramatically—up 56 basis points since April—to around 7.32% by late August, underscoring the weakness in long-duration demand and reflecting fears of mounting fiscal pressures. This rise was compounded by muted appetite from traditional institutional investors such as banks, insurers, and pension funds, whose conservative stance left demand gaps and created what analysts described as a “buyer’s strike,” particularly in longer-term securities, amplifying the supply-driven rise in yields. Investors grew uneasy following Modi’s Independence Day remarks on restructuring indirect tax slabs, which were interpreted as potentially reducing government revenue and necessitating higher borrowing; the anticipation of larger central and state debt auctions crowded the supply calendar and pushed yields higher, marking the sharpest jump in over a year. Despite this, the Reserve Bank of India (RBI) maintained a cautious but accommodative monetary stance, holding the repo rate at 5.5% and ensuring system liquidity through tools like Variable Rate Reverse Repo (VRR) and Variable Rate Repo Refunding (VRRR) auctions, while keeping core liquidity at over ₹5 trillion and surplus liquidity above ₹2.8 trillion. These interventions kept short-term money market rates steady, ensured smooth transmission of earlier rate cuts, and supported investor demand for government securities, preventing yields from spiking further. Global dynamics, however, weighed heavily: persistent US inflation delayed expectations of Federal Reserve rate cuts, keeping global interest rates elevated and narrowing the India-US yield spread to multi-decade lows, which dampened the relative appeal of Indian debt for foreign portfolio investors (FPIs). At the same time, geopolitical tensions—including the US imposition of steep 50% tariffs on Indian exports on August 27 and continuing uncertainty around India’s oil trade with Russia—added risk premiums, pressuring yields upward.Yet, despite these challenges, FPIs displayed cautious optimism in the debt segment, even as they exited equities in large numbers; net inflows into debt stood at around ₹6,207 crore in August, highlighting a relative “flight to safety” within fixed income and the attractiveness of Indian bonds given their inclusion in global indices and still-compelling yields compared to developed market peers. The biggest relief came mid-month when S&P Global upgraded India’s sovereign rating from BBB- to BBB, citing fiscal prudence and macroeconomic strength, a move that briefly softened yields and boosted confidence in both sovereign and corporate issuances, particularly infrastructure and green bonds that were increasingly coming to market. Still, cautious sentiment lingered, with markets widening the spread between the 10-year yield and the repo rate to nearly 100 basis points, effectively signalling scepticism about imminent rate cuts despite July CPI inflation being as low as 1.55%. Domestic credit conditions, strong GDP growth projections near 6.5%, and robust fiscal discipline efforts provided an anchor, but the combination of institutional reticence, heavy government borrowing supply, and global rate pressures meant yields carried a modest upward bias throughout the month. In sum, the Indian debt market in August 2025 reflected a delicate balance: on one hand, it was buoyed by RBI’s liquidity support, steady foreign inflows, and a sovereign rating upgrade that reinforced investor confidence; on the other, it faced upward pressure from fiscal concerns, weak demand for long-dated paper, heavy supply expectations, and global uncertainty tied to US tariffs and elevated international yields. The net outcome was a market that avoided disorderly sell-offs and displayed resilience, yet clearly signalled that structural challenges remain, with yields likely to stay range-bound but tilted upward in the near term as global volatility persists, government borrowing continues, and domestic institutions weigh their exposure more conservatively than in previous cycles.

In August 2025, the Indian rupee witnessed significant weakness against the US dollar, sliding to trade in the range of ₹87.5 to ₹88.33 per USD and touching fresh record lows by the end of the month as global and domestic pressures converged to weigh on sentiment, capital flows, and trade expectations. The most decisive trigger came on August 1, when the US government announced steep 50% tariffs on Indian exports, an event that immediately spurred concerns about India’s export competitiveness, widened trade deficit projections, and triggered heavy demand for dollars in currency markets. Investors, already cautious amid elevated global interest rates and slowing global growth, reacted sharply by accelerating foreign portfolio investor (FPI) outflows; by late August, FPIs had withdrawn more than $9.7 billion from Indian equity and debt markets since June, with a sharp spike in withdrawals post-tariff announcement, intensifying downward pressure on the rupee. The exodus reflected both risk aversion and a preference for safe-haven assets like the US dollar, which was strengthening globally, leading to a double blow for the rupee. On domestic front, despite positive GDP growth readings and persistently low consumer inflation, the currency found little relief as rising import bills and widening trade gaps amplified vulnerability, while the Reserve Bank of India (RBI) adopted a cautious approach, intervening intermittently to smooth volatility but refraining from aggressive defence in order to conserve foreign exchange reserves and deter speculative positioning. This policy stance allowed market forces to largely dictate the rupee’s trajectory, resulting in a steady slide that culminated in levels near ₹88.33 per USD by month-end. Market participants also noted that India’s inclusion in global bond indices and the mid-August sovereign rating upgrade by S&P Global provided temporary sentiment relief, but these positives were overshadowed by capital flight, trade uncertainty, and the broader global context of higher US yields narrowing the India-US interest rate differential to multi-decade lows. Furthermore, geopolitical tensions—including US-India trade frictions and continued uncertainty surrounding oil trade flows with Russia—added layers of risk premium that investors priced into the currency outlook. The consequence was not only a weaker rupee but also tighter external financing conditions and elevated borrowing costs for corporates and the sovereign, reinforcing the linkage between external shocks and domestic vulnerabilities. In essence, August 2025 marked one of the most volatile months for the rupee in recent history, with its depreciation driven primarily by trade-related shocks, heavy FPI outflows, and global risk aversion, only partially cushioned by RBI’s calibrated interventions, leaving the currency under sustained pressure despite India’s otherwise supportive macroeconomic fundamentals.

In August 2025, global crude oil prices moved within a relatively narrow range, reflecting a delicate balance between supply-driven pressures and demand-side uncertainties. Brent crude traded mostly between $67 and $69 per barrel indicating modest stability despite underlying volatility. The month’s price movements were shaped by a combination of OPEC+ output policies, geopolitical risk premiums, U.S. trade actions, seasonal demand dynamics, and regional consumption patterns. On the supply side, OPEC+ remained the key stabilizing force. While the alliance had previously announced moderate output hikes, actual production levels stayed around 100–102 million barrels per day, as several member states struggled to raise output further due to capacity and investment constraints. This supply discipline prevented a deeper slide in prices, countering the oversupply narrative that had emerged with OPEC+’s plan to ramp up production by nearly 548,000 barrels per day. The market thus found support from the perception that OPEC+ was still willing to defend a price floor, even as its strategy leaned more toward maintaining volumes than aggressively protecting prices. Adding to supply-side firmness was the geopolitical risk premium stemming from the Russia–Ukraine conflict. Ukrainian drone attacks on Russian oil infrastructure in August raised concerns about potential disruptions in crude supply, particularly from Black Sea terminals. These developments introduced a modest upward bias in prices, as traders priced in the possibility of temporary shortages or logistical bottlenecks. At the same time, U.S. trade policies added headwinds. The announcement of 50% tariffs on Indian exports, combined with broader trade tensions, dampened global market sentiment and injected uncertainty into the outlook for oil demand. These tariffs also indirectly influenced crude flows, as India, one of the world’s largest oil importers, faced currency depreciation and trade imbalances that weighed on its import capacity, although domestic refiners continued securing supplies from the Middle East at discounted rates. Seasonal and demand-related factors also played a crucial role. Toward the end of August, the end of the summer driving season in the U.S. typically leads to a decline in gasoline demand, and this seasonal effect contributed to softer sentiment. However, Asian demand helped counterbalance this trend. Both India and China increased crude imports in August, with total Asian purchases rising from 24.91 million barrels per day in July to 27.18 million bpd. Analysts suggested this surge was partly linked to low-price restocking rather than a clear sign of accelerating consumption, yet it nonetheless provided tangible demand support that helped keep Brent anchored in the high $60s. Broader macroeconomic and structural factors also influenced the market. Global growth concerns, especially slowing demand in advanced economies due to persistent inflation and elevated interest rates, curtailed expectations of a robust rebound in crude consumption. By the end of August, crude prices essentially consolidated within their established bands, with Brent closing near $68.5 per barrel and WTI around $64.5 per barrel. The month reinforced the theme of cautious equilibrium: supply discipline from OPEC+ and Asian buying provided floors, while U.S. tariffs, seasonal demand tapering, and slowing global growth capped the upside. Overall, crude oil in August 2025 embodied a market in balance, with geopolitical uncertainty and structural headwinds keeping volatility contained but preventing any major breakout.

The bullion market in August 2025, particularly gold and silver, experienced a phase of moderate volatility but maintained an overall stable to slightly bullish undertone, driven by global macroeconomic uncertainties, domestic demand factors, and currency movements. Gold in India largely hovered around the psychological ₹1,00,000 per 10 grams mark, reflecting resilience despite sharp intra-month swings. For instance, gold touched ₹1,01,060 on August 11, slipped to ₹1,00,520 on August 23, and then regained ground toward the end of the month. On the global front, international gold prices consolidated near $3,370 per ounce, sustaining elevated levels after a year of strong gains. A key driver behind gold’s resilience was safe-haven demand, as geopolitical tensions, including escalating U.S. tariff measures and ongoing conflicts. The rupee’s persistent weakness against the U.S. dollar, hovering near record lows around ₹88 per dollar, further underpinned domestic bullion prices by raising import costs and enhancing gold’s appeal as a hedge. Seasonal buying patterns in India also played a role, with demand beginning to strengthen ahead of festivals and weddings. The silver market displayed modest upward momentum, supported by its dual role as both an industrial metal and a safe-haven asset. Domestic silver prices climbed into the ₹1,14,000–₹1,18,000 per kg range in late August, showing relative strength compared to gold. Globally, silver advanced by about 2.2% in the last week of August, a move aided by industrial consumption trends, particularly in electronics and renewable energy, and investor allocations into precious metals amid volatility. The narrowing gold-silver ratio also signalled silver’s outperformance during the month, highlighting investor preference for the metal’s industrial-linked growth story. The sharpest bullion movements occurred between August 11 and August 14, when Indian 24K gold saw one of its steepest corrections of the year, dropping nearly ₹930 per 10 grams in just three days. This fall was largely triggered by the reversal of tariff rumours. Initially, speculation that the U.S. might impose tariffs on Swiss gold bars had driven futures higher, but President Trump’s official dismissal of those rumours on August 12 sparked a global selloff. This correction was amplified by profit booking, as gold had already surged over 28% since January 2025, recently breaching the ₹1 lakh mark in India. At the same time, the RBI’s intervention in the currency markets strengthened the rupee temporarily, lowering import costs and adding further pressure on local gold prices. Toward the end of August, however, the trend reversed again, with gold regaining strength. On August 29, international gold futures briefly touched near-record highs of $3,477 per ounce, fuelled by speculation that the U.S. Federal Reserve could consider rate cuts to cushion global growth, reigniting safe-haven demand. This late-month rally provided a bullish tone to an otherwise range-bound month. In summary, the bullion market in August 2025 was defined by stability with pockets of sharp volatility. Gold consolidated near ₹1,00,000 per 10 grams in India and $3,370 per ounce globally, supported by safe-haven demand, rupee depreciation, and seasonal domestic consumption. Silver outperformed with steady gains, benefiting from both industrial demand and safe-haven appeal. The most notable gold price move came mid-month, triggered by a reversal of tariff rumours and profit booking, while late August saw renewed bullishness on expectations of U.S. monetary easing. Overall, bullion markets in August reflected a careful balance of geopolitical risk, domestic currency pressures, investor sentiment, and seasonal consumption trends, with gold providing stability and silver showing relative strength.

In August 2025, the Indian mutual fund industry experienced a period of robust activity marked by regulatory reforms, strong performance across categories, innovative product launches, and expanding investor participation. The most significant driver was the implementation of SEBI’s new mutual fund regulations, effective from July 1, which shaped market operations through August. These reforms mandated stricter deployment of New Fund Offer (NFO) proceeds within 30 business days, required senior AMC employees to invest in their own schemes to ensure “skin in the game,” and introduced enhanced stress testing, transparency norms, and greater flexibility in investor nominations. Parallel to regulatory strengthening, the industry saw a surge in product innovation and fund launches. Between August 5 and 12, Jio BlackRock Mutual Fund, a new entrant, introduced five low-cost index fund NFOs, tracking benchmarks such as Nifty 50, Midcap 150, Next 50, and Smallcap 250, along with a G-Sec-focused debt fund, with retail-friendly minimum investments of just ₹500. Mirae Asset Mutual Fund added to the passive segment with two new index funds open from August 11 to 25, while Edelweiss launched the Multi Asset Omni Fund of Funds, diversifying across equity, debt, and commodity ETFs. A landmark moment came when Quant Mutual Fund introduced India’s first Specialized Investment Fund (SIF), offering a long-short equity strategy aimed at sophisticated investors, underscoring the industry’s push toward expanding its product suite beyond traditional offerings. Performance-wise, the industry showed remarkable strength. By mid-August, total Assets Under Management (AUM) had crossed ₹74 lakh crore, more than seven times higher than a decade ago. Equity funds remained the dominant category, accounting for nearly 60% of AUM. Several large- and mid-cap funds generated monthly returns of 12–15%, while 18 equity funds posted gains exceeding 30% since the last year, fuelling investor inflows and enthusiasm. Debt funds also saw heavy inflows, reversing earlier outflows, as investors sought stability amid global volatility. Hybrid funds maintained steady interest due to their balanced profiles, while thematic funds witnessed selective outflows, highlighting investor caution toward niche strategies. Passive funds, particularly ETFs and index funds, gained traction, making up about 17% of total AUM, as investors increasingly preferred low-cost, benchmark-aligned options. Retail participation also continued to deepen through Systematic Investment Plans (SIPs), which registered monthly contributions of around ₹28,000 crore in July. Overall, August 2025 was a transformative month for the Indian mutual fund industry, defined by regulatory reforms, record AUM growth, innovative launches, and rising investor engagement across both traditional and alternative investment avenues.